The Vix/10-yr ratio has dropped significantly since its August 24th peak, but remains quite high from an historical perspective. However, a reduced level of fear and pessimism (for which this ratio is a proxy) has corresponded to a welcome bounce in equity prices.

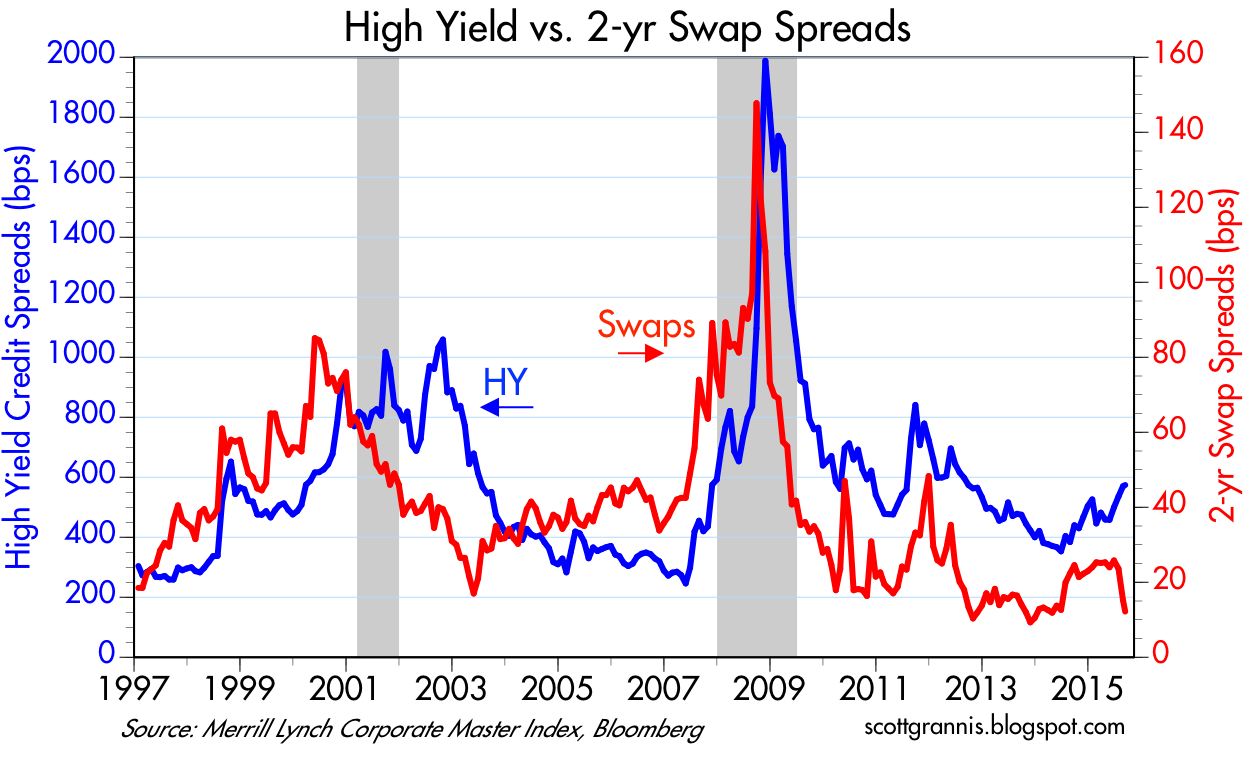

2-yr swap spreads remain quite low, suggesting that the moderate rise in high-yield credit spreads is likely to fade. In any event, the rise in HY spreads is mainly attributable to the energy sector, where a significant decline in oil prices has increased default risk.

Eurozone swap spreads remain relatively low as well. The chart above suggests that systemic risk in the U.S. and the Eurozone is low—so far there has been no contagion from the energy sector to the broader economy.

The prices of gold and 5-yr TIPS (using the inverse of their real yield as a proxy) continue to trend lower. This suggests that the world is gradually recovering some of the confidence it lost in the runup to the PIIGS crisis in late 2011. It also suggests that the fears surrounding the possible ramifications of a slowdown in the Chinese economy are relatively groundless. If the global economy were unraveling, prices of gold and TIPS would be moving higher, not lower.

0 Response to "Chart updates V"

Posting Komentar