The charts that follow illustrate the market's inflation expectations as implied by the pricing of TIPS and Treasury notes and bonds. They all show that although inflation expectations have declined somewhat of late, they are not unusually low. It's notable that inflation and inflation expectations have remained solidly above 1-1.5% for the past 5 years, despite this being the slowest recovery on record—that suggests that the Fed's concern about slow growth leading to deflation are overblown. It's also notable that inflation hasn't been a lot higher despite the Fed's unprecedented experiment with massive Quantitative Easing—that suggests that the Fed hasn't really been printing money, but rather just supplying the world with risk-free assets (i.e., bank reserves) that have been in high demand.

The chart above compares the nominal yield on 5-yr Treasuries with the real yield on 5-yr TIPS. The difference between the two (the green line on the chart) is the market's expected average annual inflation rate (CPI) over the next 5 years, which is currently about 1.6% That is lower than the 2.3% average inflation rate we've had over the past 10 years, but it is consistent with the fact that oil prices have fallen by about 30% in recent months and CPI inflation ex-energy has been running 1.5-2% for the past few years. With big declines in gasoline prices we should expect to see headline inflation fall somewhat. Moreover, there's no reason for the Fed to worry about a somewhat lower rate of inflation that is the by-product of falling energy prices, since cheaper energy should bolster economic growth.

In short, I don't see anything to be concerned about on the inflation or monetary policy front at the present time.

The chart above shows the 10-yr version of the first chart, and the green line represents the market's expected average annual CPI inflation rate over the next 10 years, which is currently about 1.8%. That too is consistent with our inflation experience in recent years and the behavior of energy prices.

The chart above effectively links the first two. It shows the implied forward-looking inflation rate five years from now (i.e., what the average annual inflation rate is expected to be from 2019 through 2024). For years 1-5, as the first chart shows, inflation is expected to be about 1.6% a year. For years 6-10, as the second chart shows, inflation is expected to be faster, about 2.2% per year. Over the next 10 years, inflation is expected to average 1.8%. That's just fine in my book, although I'd be a little happier if inflation were closer to zero. Low and stable inflation is nirvana for supply-siders, since it fosters confidence, facilitates long-term planning (which in turn boosts investment and productivity gains), and minimizes the world's need to spend time and money looking for inflation hedges. Why the Fed is so fixated on inflation being 2% instead of 1% is a mystery that can only be explained (possibly) by the Fed bowing to the current "wisdom" that low inflation exposes the economy to the "risk" of deflation. It may be politically expedient to extoll the risks of deflation, but there is no practical reason to do so. Deflation doesn't lead to slow growth, and deflation is not incompatible with strong growth.

Nothing mysterious or scary about these numbers, in any event.

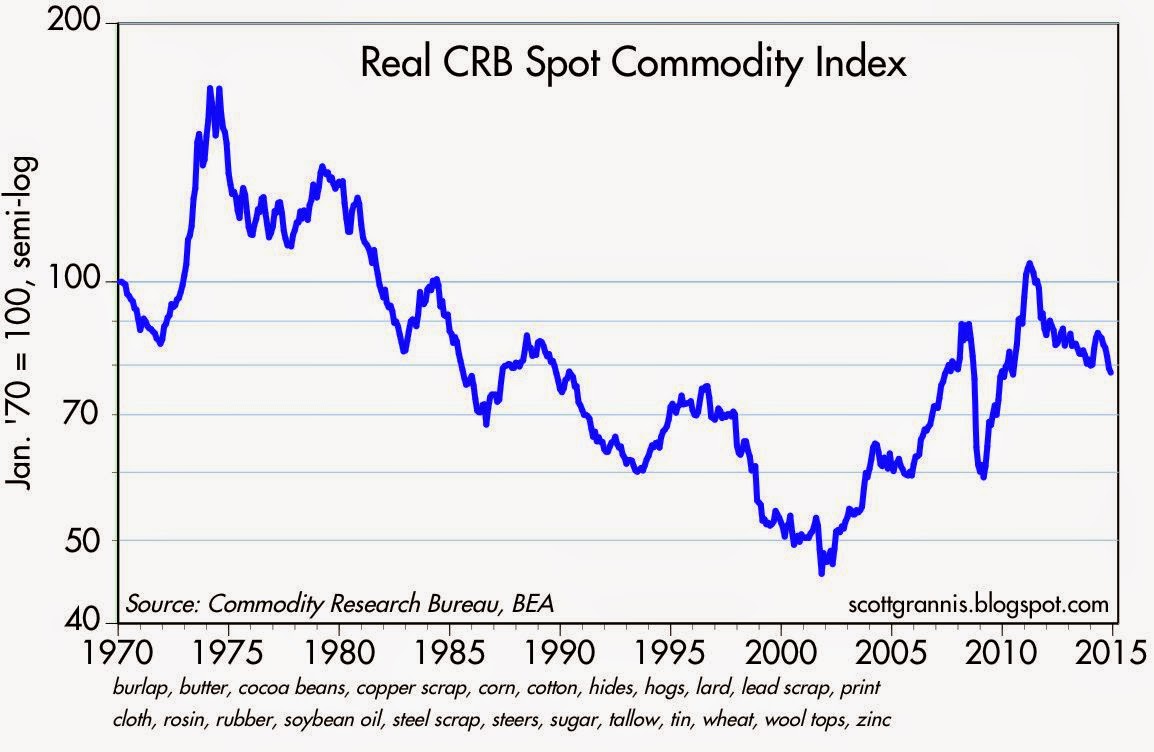

So what about falling commodity and gold prices? As I see it, commodities and gold are still trading well above the levels of 10-15 years ago. (see chart above) The next two charts look at gold and commodities in real terms, which I think is more relevant when considering whether commodity prices are likely to contribute to inflation or not.

As the chart above shows, in real terms gold is still about double what it has averaged over the past century. Today's gold prices therefore reflect a substantial premium, which in my mind means that the market still worries a lot about the possibility of the Fed making an inflationary error in the future, and the possibility of geopolitical turmoil. Gold, in other words, is still priced to a substantial risk of something going wrong. But since gold has fallen from $1900 to $1200 in the past few years, it means that the market's concerns have been alleviated to some degree. That's good. It's not a harbinger of deflation, it's a sign that the risk of high inflation has gone down.

As the chart above shows, in real terms commodity prices today are about 10% below their 45-year average. They were really cheap in 2002, and that was a time when the dollar was very strong, gold was very weak, and deflation was a definite possibility. Today, commodity prices are only somewhat lower, relative to other things, than they have been for many decades. In my view, this means commodity prices today aren't likely to impact overall inflation by much, if any.

All things considered, the near-term outlook for inflation is not worrisome at all. But I still worry that the Fed could be slow to raise short-term rates and/or withdraw excess reserves in a timely fashion should inflation begin to accelerate. In short, for now things look OK, but I still think the risk of higher inflation down the road is more worrisome than the risk of deflation.

All of this suggests that the Fed is unlikely to do anything that would shock the markets in the foreseeable future (e.g., the next 3-6 months).

0 Response to "Inflation expectations are just fine"

Posting Komentar