There's a way to judge whether monetary policy is likely to pose a threat to economic growth, and I lay it out in this post. It involves looking at the real Federal funds rate (using the Interest on Reserves that the Fed pays as a proxy), the real yield on 5-yr TIPS, and the slope of the nominal and real yield curves. If overnight real yields are high (>3%), if they exceed the real yield on 5-yr TIPs, and if the nominal and real yield curves are flat or negatively sloped, then monetary policy poses a clear and present danger to the economy. By these standards, monetary policy currently poses little or no risk to the economy. The risk of recession is consequently very low for the foreseeable future. Today's market action suggests that the market has been excessively concerned about the threat of monetary policy. That reinforces my long-held belief that the market still has a healthy amount of risk aversion, and is therefore not over priced.

When judging the impact of monetary policy on the economy, it's important to remember that the level of nominal short-term interest rates is far less important than the level of real short-term interest rates. For example, 10% nominal interest rates are far less burdensome in a world of 10% inflation than in a world of 1% inflation. The FOMC in the past has stated clearly that although its main monetary tool/target is the overnight Fed funds rate, what it is really targeting is the real overnight Fed funds rate. When they want to slow the economy and/or bring inflation down, the FOMC raises real short-term rates; when they want to "stimulate" the economy the FOMC seeks to lower real short-term interest rates.

As the chart above shows, the real Fed funds rate has been negative for the past seven years, and is currently about -1%: the difference between the 1.3% year over year rise in the PCE Core deflator, the Fed's preferred measure of inflation, and the interest rate paid on reserves of 0.25%.

So the Fed's primary policy tool is the real Fed funds rate, and that determines the risk-free yield for the front end of the real yield curve. The market's assessment of the future path of the real Fed funds rate is what determines real yields across the maturity spectrum; that in turn is a function of Fed guidance and the market's view of the future strength of the economy and the direction of inflation. If the market expects the Fed to raise real short-term yields over time, the real yield curve will be upward sloping; if the market comes to believe that the Fed will begin to reduce short-term real yields, then the yield curve flattens and eventually inverts. Fortunately, the real yield on TIPS (which are default free and inflation-protected) is a handy, liquid, and market-based indicator of the expected future path of the real Fed funds rate. In my opinion, TIPS are one of the most under-appreciated of all economic and financial indicators.

As the chart above shows, it is the combination of the level of the real Fed funds rate and the market's perception of the future direction of real yields that can tell us volumes about the health of the economy. Every recession in the past 55 years has been preceded by a significant increase in the real Fed funds rate (blue line) and a flattening or inversion of the yield curve (red line). When the market begins to sense that the Fed will eventually need to reduce real short-term rates (i.e., when the yield curve flattens and/or inverts), that is the time when monetary policy has finally begun to weaken the economy, and that in turn will force the Fed to respond with a reduction in real interest rates. Today, the real overnight rate is very low and both the nominal and real yield curves are positively sloped, so the risk of recession or even an economic slowdown is minimal, according to this model.

The chart above compares the real Fed funds rate to the real yield on 5-yr TIPS. When the real yield on 5-yr TIPS is higher than the real overnight yield, as it is today, the real yield curve is by definition positively sloped, which means the market expects that the Fed will be raising rates for the foreseeable future. It's when the real yield curve becomes inverted (when short-term real yields equal or exceed 5-yr real yields) that monetary policy becomes a threat to the health of the economy, because a flat or negatively-sloped real yield curve tells us that the market senses that the Fed can no longer raise rates and will soon have to lower them in response to a weakening economy. That (an inverted real yield curve) happened prior to both of the last two recessions, and at a time when real yields in general were much higher than they are today. Once again, the conclusion is that monetary policy today is not even remotely a threat to growth, nor is there a significant likelihood of an economic slowdown or recession.

Using the past as a guide to the future, we ought to start worrying about Fed policy only when the real Fed funds rate rises significantly and starts to approach or exceed the real yield on 5-yr TIPS. Today, that means the Fed could raise the interest rate it pays on reserves by 50 or 75 bps without threatening the health of the economy. The Eurodollar futures market says the Fed won't raise its target rate by that much until about a year from now. If by that time the economy has gathered a bit more steam and/or real TIPS yields have increased, then even a 0.75% or 1% Fed funds rate a year from now (which would equate to a real Fed funds rate of -0.5% or -0.3%) shouldn't be a problem at all. Monetary policy would still be "easy."

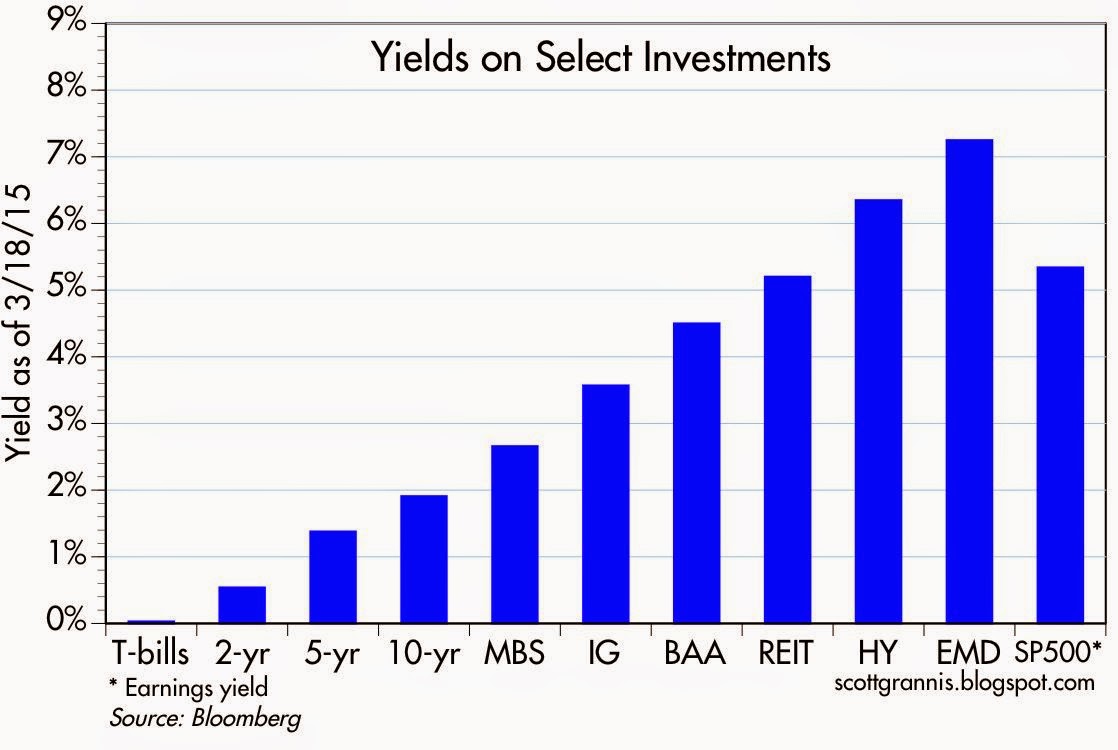

For investors, this strongly suggests that cash and cash equivalents are an inferior asset class. Yields on almost all other asset classes are substantially higher, and likely to remain so for the foreseeable future because of the low risk of an economic slowdown or recession.

0 Response to "How to know if Fed policy is a threat to growth"

Posting Komentar