The prevailing inflation meme is that it is dangerously low, and for years central banks have been trying very hard—without much success—to get it to rise. The reality—at least in the U.S.—is that the underlying "core" rate of consumer inflation has been running at close to 2% for over a decade. Energy prices have been the principal cause of variations from this trend.

Here are some charts to prove the point:

The "core" rate of CPI inflation has been far less volatile than the total rate of CPI inflation. The first of the above two charts show the year over year change in the CPI and the CPI Core indices. The second focuses on the 6-mo. annualized change in these same indices. The total rate of CPI inflation was about zero over the past six months, but it grew at a much more rapid 3.18% (annualized) rate over the past three months. In other words, the overall CPI is quickly "catching up" to the CPI Core and CPI ex-energy rate of inflation, and all are covering at something in the range of 1.8-2.0%.

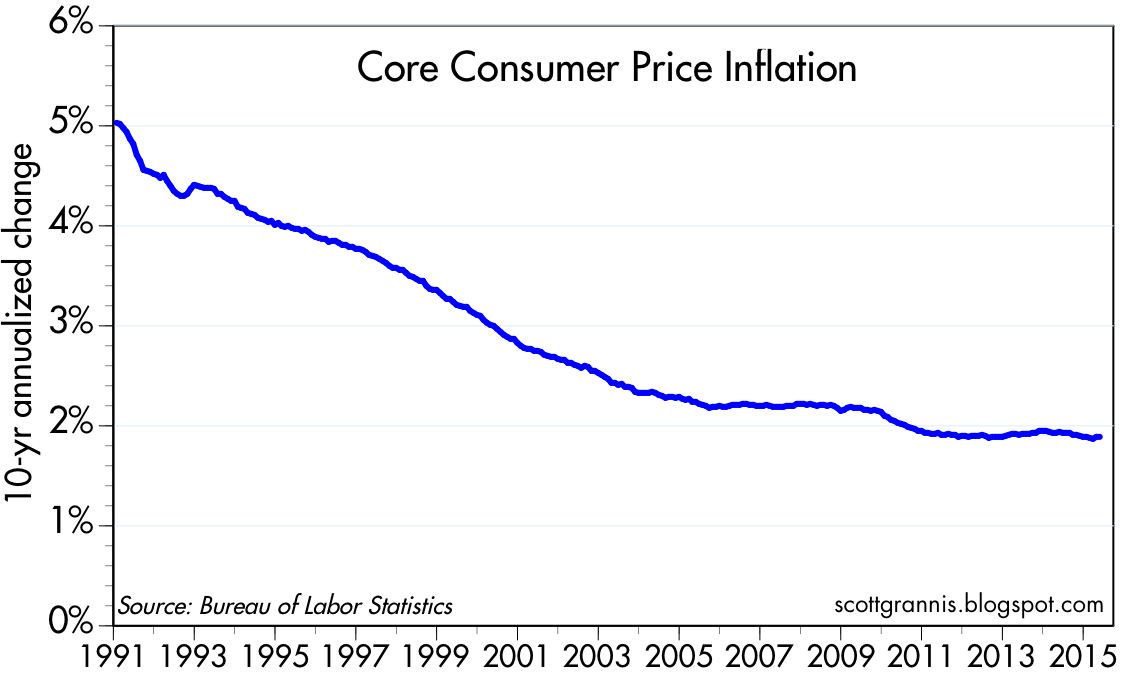

The chart above shows the 10-yr annualized change in the Core CPI. By this measure, the Core CPI has been running very close to 2%, on average, for the past 14 years.

The CPI ex-energy has also been running very close to 2%, on average, for the past 12 years, as the charts above show. Over the past 10 years, the annualized rate of inflation by this measure has been 1.99%. Over the past year, it was 1.71%.

This last chart looks at the long-term trends of the CPI ex-energy. In the past decade it has been relatively low and stable, much as it was in the first half of the 1960s.

As the chart above shows, inflation as measured by the CPI and the PCE deflator has been almost the same. Over the past 20 and 30 years, inflation according to the CPI has tended to register about 40-50 bps higher per year than the PCE deflator. Thus, if the CPI continues to run at just under 2%, the PCE deflator (and its core version) will very likely run about 1.5% per year. There is nothing scary or worrisome about either of those numbers.

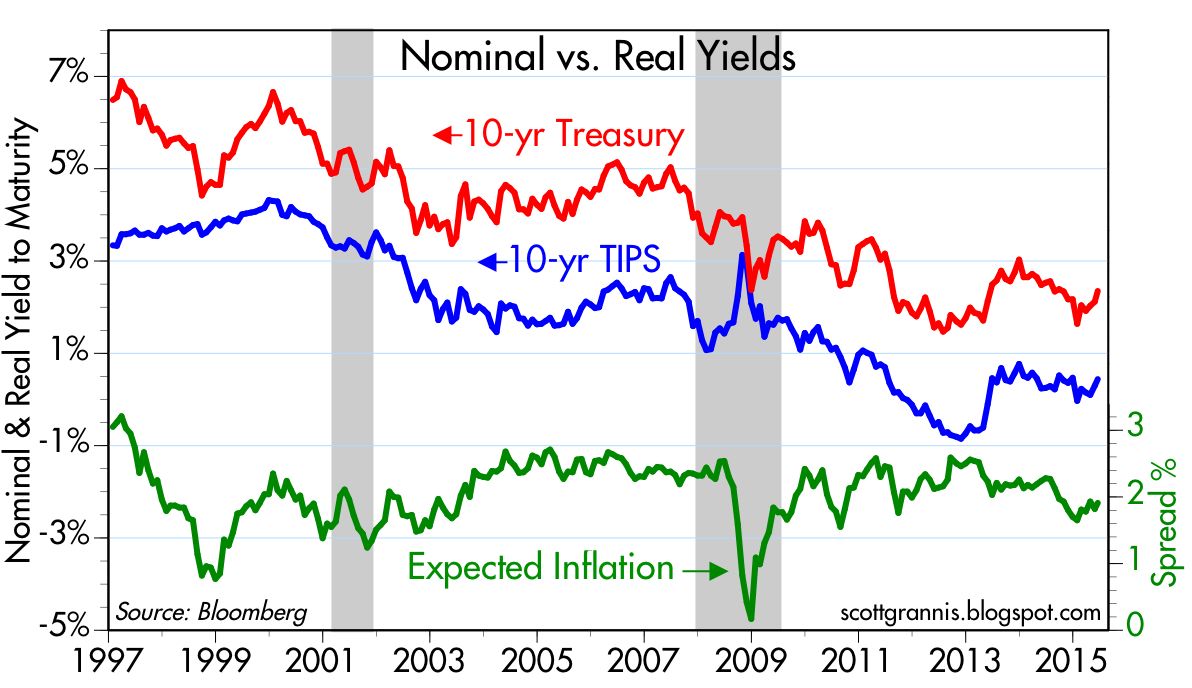

UPDATE: The bond market is currently priced to this same conclusion: consumer price inflation is very likely to be just under 2% for the foreseeable future.

The bond market currently is priced to the expectation that the CPI will average 1.72% over the next 5 years.

The prices of 10-yr TIPS and 10-yr Treasuries reveals that the market expects the CPI to average 1.91% over the next 10 years.

0 Response to "Consumer price inflation is still running almost 2%"

Posting Komentar