It's no secret that the Fed will begin raising short-term interest rates before too long. However, the method they will use has never been tried before, so there naturally exists a degree of confusion and uncertainty surrounding the future course of monetary policy and how it will affect the economy. The purpose of this post is to simplify the issue in the hope that leads to better understanding.

As I've argued in numerous posts over the past 5-6 years, the most important driver of monetary policy from late 2008 until recently has been unusually strong money demand. As I see it, the Fed was almost compelled to resort to Quantitative Easing in order to satisfy the world's demand for money and near-money substitutes. QE was not about pumping money into the economy, it was all about satisfying the economy's demand for liquidity. QE was erroneously billed as "stimulative," since printing money in excess of what's needed only stimulates inflation. Instead, QE was designed to accommodate intense demand for money, without which the economy might well have stumbled.

It all started when financial markets teetered on the edge of the abyss in the third quarter of 2008. The problem was that the world suddenly wanted a lot more money and money substitutes (e.g., cash, bank savings deposits, T-bills) than were available. Debt that made sense when housing prices were rising suddenly became suspect as prices collapsed. Too many people tried to rush for the exits, but the financial system lacked the necessary liquidity to allow so many to sell so much. Even before the meltdown that followed the collapse of Lehman, demand for T-bills was so intense that the Fed all but exhausted its holdings of T-bills by mid-2008 in an attempt to increase their supply on the market.

Such was the shortage of money in late 2008 that the dollar soared, commodity prices collapsed, and the prices of TIPS and Treasuries signaled impending deflation on a massive scale, as the charts above show.

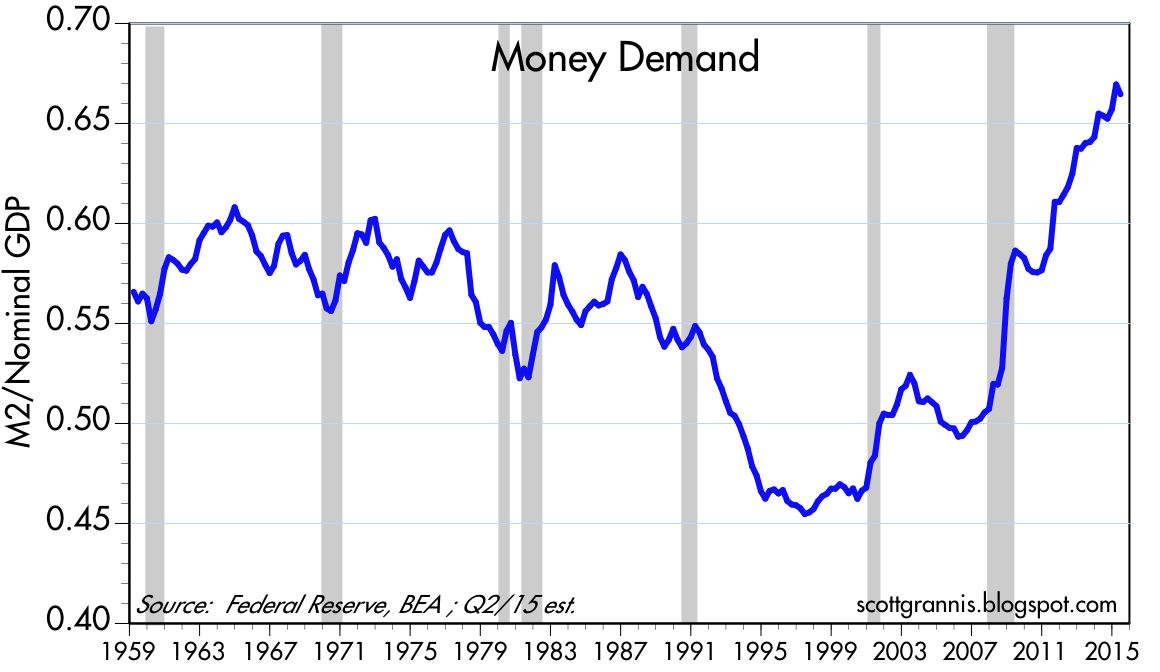

The increase in the demand for money can also be seen in the chart above, which measures the ratio of M2 (cash, demand deposits, retail savings accounts) to nominal GDP. Think of it as the amount of cash and cash equivalents that the average person wants to hold relative to his annual income. Between the end of 2007 and today, that ratio has jumped by over 30%. It's as if collectively we wanted to stuff almost $3 trillion under the mattress for a rainy day. The shock of the 2008 financial collapse and the deep recession that accompanied it resulted in years of risk aversion.

The most important policy change that QE brought with it was the Fed's decision to pay interest on bank reserves (IOR). Prior to that, bank reserves paid no interest, but banks were compelled to own them in order to collateralize their deposit base (our fractional reserve banking system required banks to hold about $1 in reservers for every $10 in deposits). This meant that reserves were a deadweight asset, so banks always tried to minimize their holdings of reserves. With QE, the Fed had to encourage banks to hold reserves, and IOR was the key to doing that.

Controlling and limiting the supply of reserves was the Fed's primary policy tool prior to QE. The Federal Open Market Committee controlled the supply of reserves indirectly, by targeting the interest rate that banks paid each other to borrow or lend the relatively fixed supply of reserves in existence. If the interest rate on the Fed funds market slipped below the FOMC's target, then the FOMC would deduce that reserves were in over-supply, and they would sell bonds in order to reduce the supply of reserves. If the Fed funds rate exceeded the FOMC's target, they would buy bonds in order to alleviate the shortage of reserves. (The Fed can only buy bonds from participating banks, and it can only pay for them by crediting the banks' reserve account at the Fed.) If the Fed wanted to ease monetary conditions, it would lower the funds rate target, and sell bonds to add reserves in order to make reserves more plentiful. By targeting the Fed funds rate and indirectly the supply of bank reserves, the Fed was thereby able to control the money supply and in turn inflation.

But paying interest on reserves changed everything. Suddenly banks viewed reserves as functionally equivalent to T-bills: a very safe, short-term, very liquid, and interest-bearing asset. If the world wanted tons of safe "money," the Fed now had the means to deliver what the world wanted. With QE, the Fed effectively transmogrified trillions of notes and bonds into T-bill equivalents. IOR allowed the Fed to create virtually unlimited supplies of the "money" that the world so desperately wanted—without being inflationary. Inflation, as Milton Friedman taught us, only happens when the supply of money exceeds the demand for it. QE was not about artificially pumping up the supply of money, it was about providing the money that the world wanted.

Banks have taken in almost $4 trillion of savings deposits since late 2008, and instead of lending all that money to the private sector, they lent most of it to the Fed, receiving bank reserves in exchange. (In practice, banks used their deposit inflows to purchase notes and bonds which they then sold to the Fed, which the Fed paid for with bank reserves.) Banks were very reluctant to lend to the private sector, but they loved lending to the Fed, since that involved zero risk.

Today we know that all of the above is true, because the Fed has purchased some $3 trillion of notes and bonds yet inflation has remained relatively low and stable. The Fed supplied just enough money to satisfy the world's demand for money, so it wasn't inflationary.

So now we look ahead to the unwinding of all this. Since a huge demand for money is what led to QE, the reversal of QE will (or at least should) be led by a reduction in the world's demand for money. If and when the banking system's desire to hold trillions of excess reserves declines, the Fed is going to have to reduce the supply of reserves—by selling its holdings of Treasuries and MBS, or allowing them to mature—and/or take steps to increase banks' desire to hold those reserves—by raising the interest rate it pays on reserves. As the Fed has told us, they will almost certainly do both, with an initial emphasis on raising the interest paid on excess reserves (IOER). If they don't, then the supply of money will exceed the demand for it, and higher inflation will ensue. Given that banks currently hold about $2.5 trillion of excess reserves, they have a virtually unlimited ability to increase their lending activities.

There's already mounting evidence that banks have returned to the lending business with gusto—which implies that the demand for money is declining and risk aversion is receding. As the chart above shows, bank lending to small and medium-sized businesses has been increasing at strong double-digit rates since early last year. Over the same period, total bank credit has increased by more than $1.1 trillion, and is growing at a 7-8% annual pace. Prior to the beginning of last year, it took almost six years for bank credit to increase by $1 trillion. From the end of 2007 to the end of 2013, it was a time of strong money demand and pervasive risk aversion. For the past 18 months, the tide has begun to turn: money demand is down and risk aversion is receding.

When banks lend more and the private sector borrows more, that is by definition a decline in the demand for money, and it goes hand in hand with a decline in risk aversion. As banks realize that lending to the private sector produces risk-adjusted returns that exceed the IOER (now a mere 0.25%), their desire to sit on mountains of excess reserves that could be used to collateralize more lending is going to decline and lending is going to accelerate further. Raising IOER makes bank reserves more attractive, offsetting banks' growing lack of interest in sitting on excess reserves.

The Fed is going to have to react to the decline in money demand which is already underway, no question. They are going to have to slowly drain reserves from the system, and they are going to have to raise the interest they pay on reserves. But it needn't be scary.

Raising interest rates a few notches at this point is not equivalent to "tightening" monetary policy. It's more like easing off the accelerator, having reached the speed limit. As the chart above suggests, "tightening" monetary policy involves increasing real interest rates. Every recession in the past 50 years has been preceded by a significant rise in real short-term interest rates and a flattening or inversion of the real and nominal yield curves. We're still years away from that happening, and real short-term interest rates (the red line in the chart) are still negative.

The Fed can raise rates by hundreds of basis points without damaging the economy or threatening the health of financial markets, because higher rates will be a natural response to a stronger economy and a decline in the demand for money. If they don't they risk a potentially painful increase in inflation.

0 Response to "The Fed's game plan: it's all about the demand for money"

Posting Komentar